Identity theft can be a dire situation. More than 40% of Americans have fallen victim to this crime. Usually, a bad actor hacks into your bank account, takes out loans in your name, or opens and maxes out credit cards. But there are more intricate schemes happening that may shock you. Here we’ll take a look at seven schemes that you need to protect yourself against.

1. The Fake Hostage Scam

Have you heard about this scam where someone calls saying that they have a loved one held hostage? One Indiana woman fell for the scam because she heard screaming in the background. The scammers demanded $1,500 be sent to their Venmo or they would shoot her mother. This scam takes many forms and sometimes scammers say that your loved one has been in a terrible accident and they need money for their care. It’s always a good idea to verify the situation before sending any money.

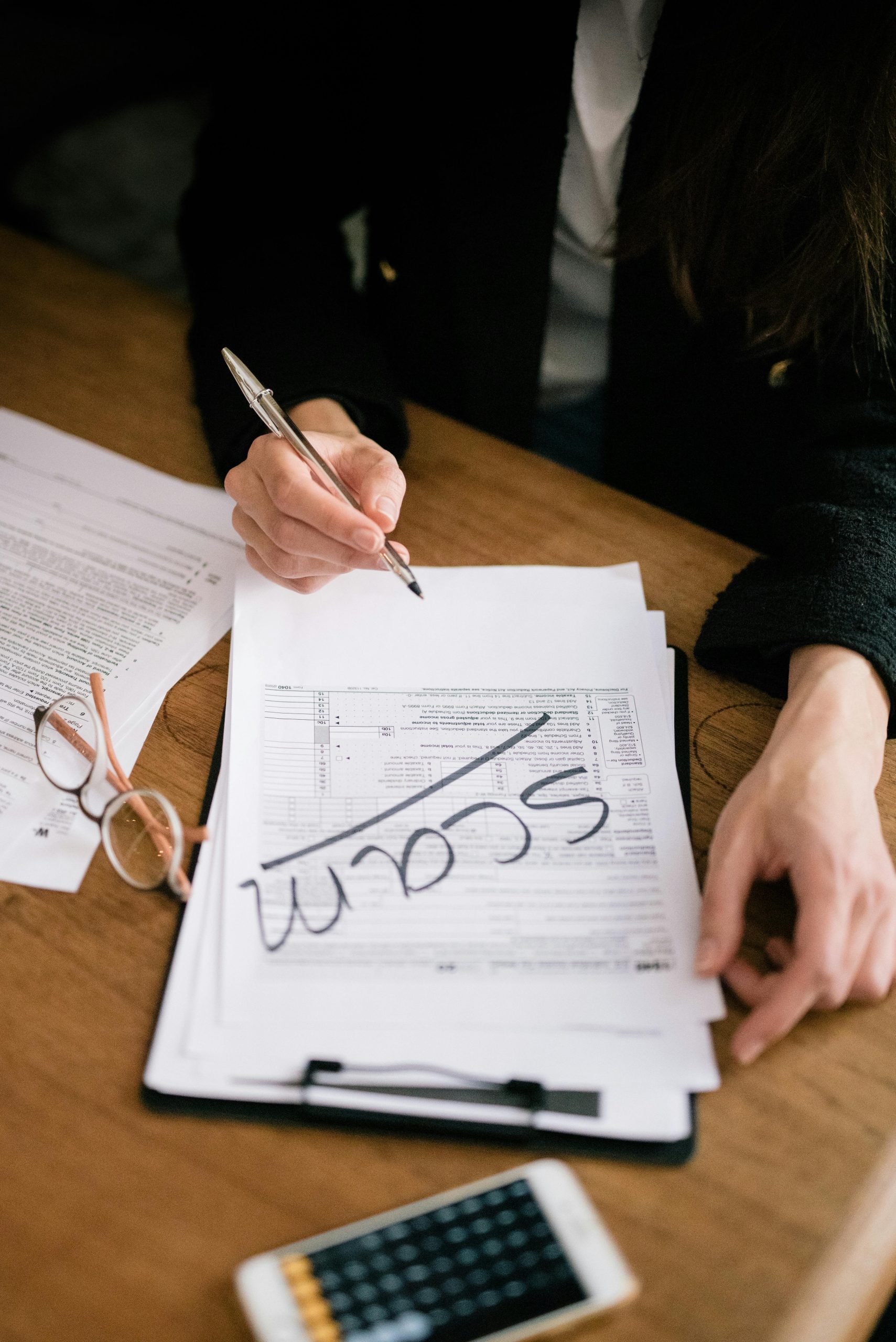

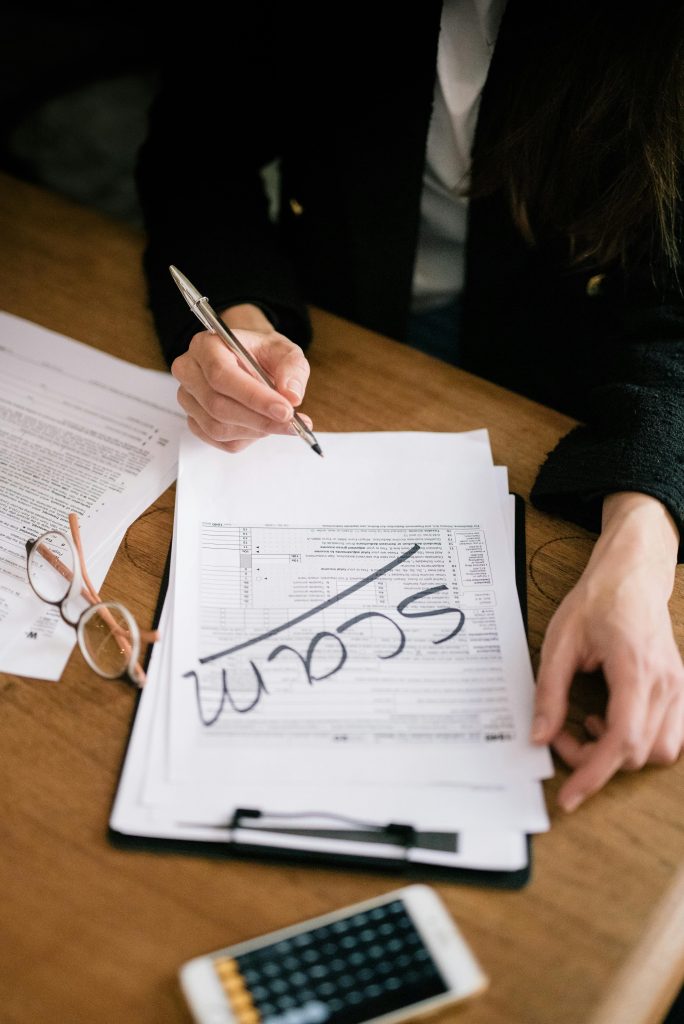

2. Scamming Lovers

Image Source: Pexels

Have you seen the Netflix documentary, The Tinder Swindler? Shimon Hayut is a skilled con artist who posed as a wealthy businessman, making many women fall for him. He would then say that business rivals were threatening his life and he needed credit cards and loans. Of course, he maxed out the credit cards and defaulted on the loans leaving his victims in financial ruin. It’s estimated that he swindled around $10 million from his targets. Hayut’s scam is similar to many romance scams that many individuals fall for every day. If your online lover starts asking for money, it’s time to move on.

3. Re-routing The Mail

Do you get a barrage of emails from companies asking if you want to have your bills sent to you paperlessly? You probably should take them up on online billing because of this scam. Abraham Abdallah was able to reroute mail and packages of more than 200 rich and famous celebrities, including Oprah and Spielberg, just by changing their mailing addresses to fake addresses around New York. He allegedly used web-enabled mobile phones and virtual voicemail services to track packages ordered by his targets and pick up messages from anywhere. Abdallah obtained banking information, social security numbers, and credit card accounts of victims for more than six months. He even tried to transfer $10 million out of Thomas Siebel’s account, founder of Siebel Systems. While mail scams are usually not this grandiose or successful, be careful what you send in the mail to protect yourself from identity theft.

4. Children as Targets of Identity Theft

Have you heard about the story of the mother who posed as her daughter so that she could go back to high school? Wendy Brown stole her daughter’s identity and attended a new high school so that she could be on the cheer team. Only 15 days later, she was sentenced to jail time. While moms don’t often impersonate their children, child identity theft has become a common phenomenon. Usually, scammers use children’s social security numbers to open credit cards, take out loans, or file fake tax returns. Children’s identities are much easier to steal than adults’. If you notice that your child is receiving offers for credit cards or not age-appropriate mail, take a look at their credit report and consider freezing it.

5. Swapping Phone Numbers

Youtuber Jacy Erin’s parents fell victim to identity theft when her mom’s email was hacked. The hackers were able to obtain sensitive information like her phone number and credit card information. They changed her mother’s phone number before putting $40,000 in charges on her credit card. When the credit card company called to confirm the charges, the call went right to the hackers.

6. Insider Job

Philip Cummings pleaded guilty in 2004 to one of the largest identity theft cases in the United States. Cummings worked for Teledata Communications, a company that helped run routine credit score checks for other companies. When Cummings quit his job he also took the passwords of 33,000 customers. He then sold the information to criminals. Through drained bank accounts and credit card charges, it’s estimated that victims of this scheme lost $50-$100 million. While breaches of this kind are historic, data breaches happen every day. If you are notified of a data breach where your information may be affected, be sure to set up a credit monitoring service to protect yourself.

7. PayPal Scheme

Just like Cummings, an IT professional Kenneth Gibson took private information he had access to from his employment. He created software that would create fake PayPal accounts for thousands of people. He then used the PayPal accounts to create new credit accounts. He flew under the radar for a while because he would only transfer small amounts of money, but in total, he stole more than $3.5 million.

Protecting Yourself from Identity Theft

According to recent data from the Federal Trade Commission (FTC), over 1 million cases of identity theft are reported each year. It’s estimated that millions more cases go unreported each year as well. While identity theft is a common crime, there are steps you can take to protect yourself. Always remember to monitor your credit card, bank statements, and credit score. You may also want to set up a monitoring service. With knowledge and the right tools, you can protect your identity from criminals.

Did you know that according to The Social Security Administration, 1 in 4 workers will become disabled during their working years? If you sustain a disability, both state or federal disability insurance and private disability insurance are viable options to lessen your economic hardship. Navigating the intricacies of disability insurance can be quite challenging so we’ll give you an overview of your options to know which is best for you.

State Disability Insurance

State disability insurance is only available in select states including California, Hawaii, New Jersey, New York, and Rhode Island. These programs are for claimants who are totally disabled claimants on a short-term basis. Each state has different requirements to be eligible for their disability insurance programs. Some typical parameters for eligibility include the length of time you have worked for your employer, how long you’ve been disabled before you can apply, and what percentage of your salary will be paid out. If your state doesn’t offer insurance, you may qualify for federal Social Security Disability Insurance.

Social Security Disability Insurance

Social Security Disability Insurance (SSDI) is only available to those who have paid into it. This means that you have contributed through payroll deductions. SSDI is available for people with both short-term and long-term disabilities. According to The Patient Advocate Foundation, “To receive SSDI, your application must show that you can no longer work in your previous occupation, you cannot adjust to a new work environment, and your disability prevents you from being able to return to work for at least a year.” There are no time limits for how long you can receive benefits.

Private Insurance

Private insurance is paid for by the employee in the form of premiums, usually collected monthly or deducted from your paycheck. Private companies sell many different types of disability insurance, so it’s important to review your plan. Most private insurance will allow for partial disability. Unlike SSDI, there usually are time limits for how long you can receive benefits for private insurance, depending on whether you have short-term disability or long-term disability insurance.

Since most private insurance is tied to your employer, see if you can take your insurance policy with you if you leave your employer. If your private insurance is portable, you’ll continue to pay the premium, even if you leave your job.

Can I Receive Multiple Benefits?

Image Source: Pexels

Yes, in some cases you can receive benefits from SDI or SSDI and private insurance. The amount that you receive from SSDI or state disability insurance will not decrease. However, private insurance policies may decrease your payout of benefits based on the amount that you are receiving from state disability insurance or SSDI. So, your monthly amount of benefits may be the same. Again, every private plan is different so contact your insurance company about your plan.

Are Benefits Taxable?

SSDI are typically not taxable income. The same is true for state disability insurance. If you are receiving unemployment benefits when you apply for disability however you may be taxed. This is because unemployment benefits are taxable and your disability insurance is seen as a substitute for you unemployment benefits. Private disability insurance is also not taxable because your premiums are paid with wages that have been taxed.

Can I Transfer My Policy?

As a rule, disability insurance can’t be transferred to another person. It is possible to designate a representative who manages your care. They may need to be interviewed or go through additional steps to manage your benefits for you.

If you move, your SSDI can be transferred to a new state. Of course, state disability insurance requires you to live in eligible states. Private insurance should also be notified of a move.

Choosing The Right Disability Insurance

Image Source: Pexels

Now that you have an overview of the insurance options that may be available to you, you can make an informed choice about which is best for you. You can always contact your state or social security office for more information about state and federal programs. An injury lawyer or your employer’s HR department may also be able to assist you.

Especially with inflation, many Americans are trying to cut back on spending. A 2023 Experian study found that 66% of Americans actively seek ways to trim expenses from their monthly budget. But what if we told you that some of your money-saving habits are actually costing you money? You could be approaching saving money all wrong. Let’s take a look at your money-saving strategies and whether or not they’re actually costing you more than they save.

1. Ignoring Price Per Unit

Image Source: Pexels

I am personally guilty of this. When money is tight, I tend to buy the cheapest things I can find at the grocery store. That said, I often fall into the trap of buying small quantities that are actually more expensive than if I spent a few more dollars on larger quantities. So, it’s important to look at the price per unit to determine if the item you’re buying is actually a good deal. Otherwise, your money-saving strategy could be costing you more in the long run.

2. Overbuying in Bulk

Image Source: Pexels

The same is true for buying everything in bulk. First, what is realistic for you and your family to use or consume before the product spoils or expires? Then, do a little math and make sure that the bulk price is really saving you money. Many stores like Costco, Sam’s Club, and BJ’s don’t have amazing deals on everything just because they are bigger quantities. To get the best deals on items, research prices on Flipp to see prices at other stores in your area.

3. Just Buying Something Because It’s on Sale

If you’re only buying items on sale, you might actually be paying more. For example, a name-brand peanut butter on sale could still be more expensive than the store brand. Additionally, if there is a sale in-store it’s likely that you can save even more by stacking manufacturer coupons and rebates on apps like Rakuten, Ibotta, Shopkick, and Fetch. Check out videos on social media from well-known couponers for the best tips.

4. Hanging onto an Old Car

If you just bought an old car or are hanging onto a clunker, you may be wasting money. Gas mileage alone on an older car could be costing you money. Plus, if you’re putting money into repairs, you are probably spending more than the car is worth.

5. Avoiding Doctors and Dentists

Image Source: Pexels

While paying for insurance deductibles is expensive, ignoring preventative care isn’t a good money-saving strategy. You could be missing treatable health conditions by putting off visits to the doctor or dentist. While no one likes going to the dentist, good oral health can health prevent costly procedures like root canals.

6. Ignoring Quality of Purchases

Just because the clothes on Shein are inexpensive doesn’t mean that they are a good deal in the long run. If you consider cost per wear, a better quality garment may be worth the investment. You can always get better quality clothes at the thrift store or on the resale market to cut costs. The same is true for household items. There are things you should invest in so that they stand up to wear like quality pots and pans.

7. DIYing Repairs

Image Source: Pexels

It’s tempting to think that you can save money on home repairs by doing it yourself. Yes, professionals are expensive, but larger projects often require an expert’s knowledge and skill. So, next time you have a leak in your roof, don’t try and fix it yourself unless you are equipped to do so. Any mistakes you make could cost you a lot more to rectify.

Reevaluating Your Money-Saving Strategy

Sometimes saving more money is about changing your mindset. Spending the least amount of cash doesn’t mean that you’re saving money in the long run. You may actually be paying more for simple things like grocery items if you buy smaller quantities. Or if you have to replace a winter jacket every year because you purchased one that was poor quality over time you are probably spending more money. So, make your purchases wisely and do your research to get the best deals that actually save you money.

What is your best money-saving strategy? Let us know in the comments.